Final Regulations Released for Partnership Recourse Liabilities

Tax

12.20.24

On December 2, 2024, the Department of Treasury published final regulations (Final Regulations) governing the allocation of recourse liabilities of a partnership among its partners under Section 752 of the Internal Revenue Code of 1986, as amended. The Final Regulations adopt, with certain modifications, proposed regulations previously issued in December 2013.

The new guidance contained in the Final Regulations focus principally on the following:

- Resolving certain uncertainties regarding which partner or partners are considered to have “economic risk of loss” (EROL) with respect to a recourse liability of the partnership, including how a recourse liability should be allocated among multiple partners who each bear EROL

- Addressing the allocation of recourse liabilities in tiered partnership structures

- Clarifying how to apply related-party rules to allocate partnership recourse liabilities, including ordering rules when multiple related-party relationships exist.

For the purposes of these rules, a liability is considered a “recourse liability” if one or more partners bear EROL with respect to such liability. Recourse liabilities are allocated among partners based on their respective EROL. Most typically, a partner is considered to have EROL with respect to a partnership liability if (i) the partner (or a person related to that partner) guarantees the liability (in whole or in part), or (ii) the partner (or a person related to that partner) is the lender because, in either case, that partner would suffer an economic loss (e.g., a guaranty obligation or bad debt loss) if the partnership does not fully repay the liability.

The Final Regulations are generally effective for liabilities incurred or assumed on or after December 2, 2024. If a liability incurred before December 2, 2024 is refinanced on or after that date, the rules in the Final Regulations will generally apply only to any increase in the amount of the liability or to the extended term.

Multiple Partners with EROL

In certain situations, multiple partners might bear the EROL with respect to a recourse liability of a partnership. Examples include arrangements where multiple partners each provide a guarantee (in whole or in part) for a partnership liability, or where one partner is the lender and one or more other partners provide guarantees (in whole or in part).

The Final Regulations adopt the proportionality rule in the proposed regulations for determining how partners share a recourse liability when multiple partners bear EROL for that liability. Under this rule, each partner’s EROL with respect to the recourse liability (or portion thereof) is multiplied by a fraction where (i) the numerator is the amount of EROL borne by that partner and (ii) the denominator is the sum total of EROL with respect to that liability borne by all partners.

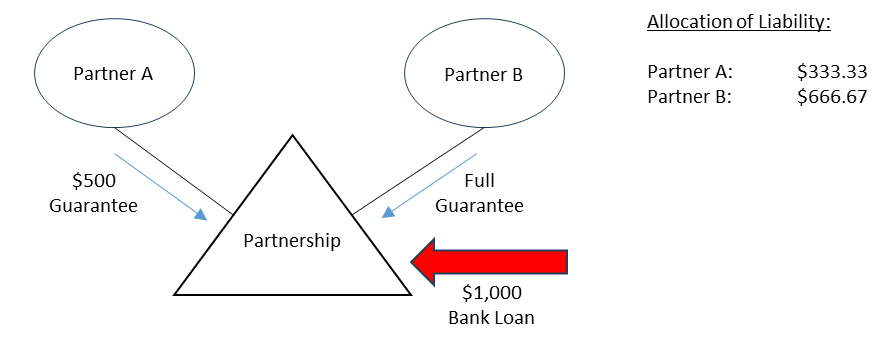

Illustrative example:

Partner A and Partner B are both partners in the Partnership. The Partnership borrows $1,000 from a third-party bank. Partner A guarantees $500 of the loan, and Partner B guarantees the full amount of the loan. In this case, Partner A’s share of the recourse liability would be $333.33 (Partner A’s $500 EROL divided by the partners’ combined $1,500 EROL), and Partner B’s share would be $666.67 (Partner B’s $1,000 EROL divided by the partners’ combined $1,500 EROL).

Tiered Partnerships

The Final Regulations also contain updated rules for allocating recourse liabilities in a tiered partnership structure,e.g., where an upper-tier partnership (UTP) is itself a partner in a lower-tier partnership (LTP). In general, the LTP must allocate to the UTP the portion of any LTP recourse liability for which the UTP or any partner of the UTP bears EROL. However, if a partner of the UTP who bears EROL with respect to the LTP’s liability is also a partner in the LTP, then the LTP directly allocates to that partner the portion of the LTP’s liability for which the partner bears the EROL.

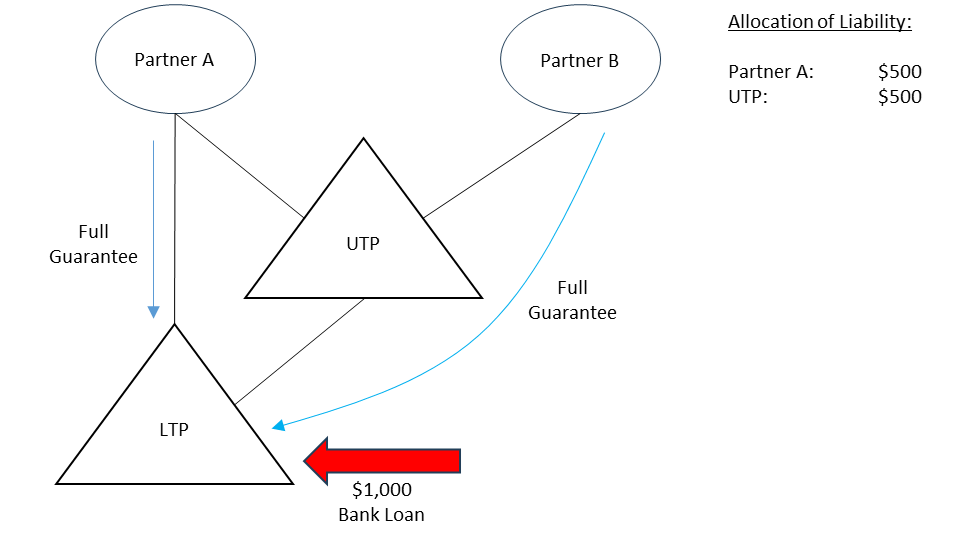

Illustrative example:

Partner A and Partner B are both partners in UTP. Partner A and UTP are also partners LTP. Partner B is not a partner in LTP. LTP borrows $1,000 from a third-party bank. Each of Partner A and Partner B provides full guarantees for LTP’s loan. Under the Final Regulations, Partner A’s share of the LTP liability is $500 (Partner A’s $1,000 EROL divided by Partner A’s and Partner B’s combined $2,000 EROL) and LTP directly allocates that share to Partner A because Partner A is also a partner in LTP. Partner B’s share of the liability is also $500 (Partner B’s $1,000 EROL divided by Partner A’s and Partner B’s combined $2,000 EROL), but Partner B is not a partner in LTP. Therefore, LTP allocates Partner B’s $500 share of the liability to the UTP.

Related Party Rules

Under Section 752, a partner that does not directly bear any EROL can nonetheless be treated as bearing EROL with respect to a liability if a related party to such partner bears EROL. Determining whether a partner might have an indirect EROL in these situations can be quite challenging as a result of the application of certain constructive ownership rules, which govern when a partner and another party might be related for this purpose. The Final Regulations help clarify the related party rules in a few ways.

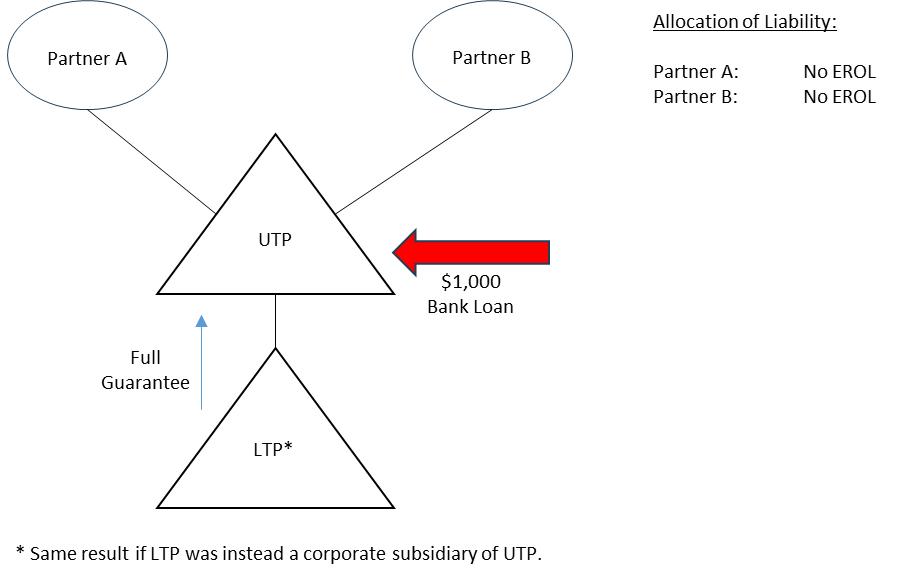

First, the new rules provide that a partner is not treated as bearing EROL with respect to a liability of a UTP when an LTP or a corporate subsidiary of the UTP directly bears EROL (e.g., the LTP or corporate subsidiary provides a guarantee or is the lender). In those situations, partners in the UTP are not considered related to such LTP or corporate subsidiary merely by virtue of indirectly owning such LTP or corporate subsidiary through their UTP interests. The Final Regulations accomplish this by turning off certain partnership interest and stock ownership attribution rules that might otherwise apply.

Illustrative Example:

Partner A and Partner B are both partners in UTP. UTP is a partner in LTP. UTP borrows $1,000 from a third-party bank. LTP provides a full guarantee for UTP’s loan. Under the Final Regulations, LTP is not considered related to either Partner A or Partner B under these facts. Therefore, neither Partner A nor Partner B bear EROL with respect to UTP’s liability.

Next, if a direct or indirect partner of a partnership directly bears EROL for a recourse liability of a partnership, other direct or indirect partners in that partnership are not treated as related to such partner for purposes of determining the EROL (if any) of those other partners. In general, these rules serve to prevent a partner from being treated as indirectly bearing EROL as a result of its related party status with another partner that directly bears EROL.

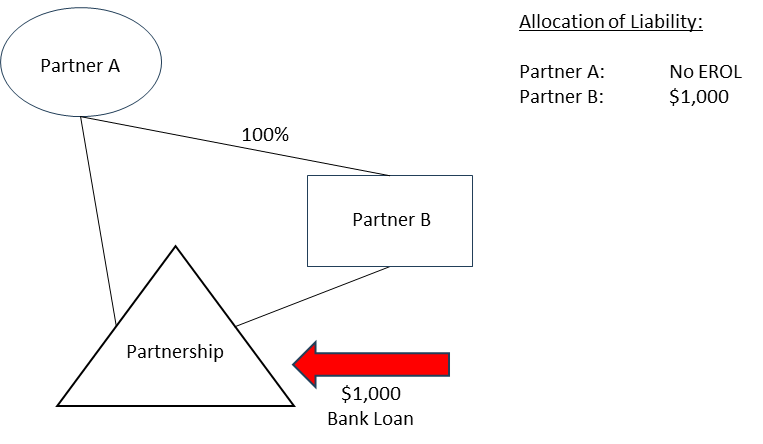

Illustrative Example:

Partner A and Partner B are both partners in the Partnership. Partner A also owns 100% of Partner B, which is a corporation. Partnership borrows $1,000 from a third-party bank. Partner B provides a full guarantee for Partnership’s loan, and Partner A provides no guarantee. Since Partner B is a direct partner in the Partnership and has direct EROL with respect to the liability, Partner A, which does not have direct EROL, is not considered related to Partner B. Accordingly, Partner A is not considered to bear EROL with respect to the liability, and the liability is allocated entirely to Partner B.

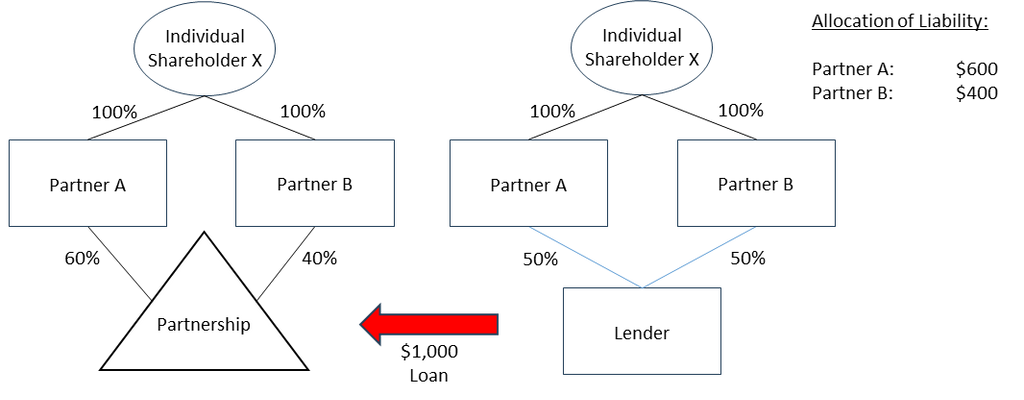

Finally, if multiple partners are related to a non-partner that directly bears EROL with respect to a partnership liability, the related partners are treated as bearing EROL in proportion to their interest in the partnership’s profits.

Illustrative Example:

Individual Shareholder X owns 100% of each of Partner A and Partner B, which are both corporations. Partner A and Partner B hold, respectively, 60% and 40% of the interests in the Partnership. Partner A and Partner B also each owns 50% of the stock of the Lender, which is a corporation as well. The Partnership borrows $1,000 from the Lender. Under the relevant related party rules, each of Partner A and Partner B is considered related to the Lender, which is not a partner in Partnership. Accordingly, Partner A and Partner B are considered to bear EROL with respect to the liability in accordance with their interests in the profits of the partnership (i.e., 60% for Partner A and 40% for Partner B).

Conclusion

The allocation of recourse liabilities of a partnership can have significant economic implications for partners. For instance, a partner’s tax basis in its partnership interest will generally be increased by the amount of the partner’s share of a recourse liability, which can permit such partner to receive more cash distributions from the partnership without recognizing immediate taxable income or allowing such partner to deduct more expenses or losses allocated to it from the partnership.

The Final Regulations therefore provide welcome clarity and additional guidance regarding the allocation of partnership recourse liabilities, albeit more than a decade after the proposed regulations were first issued. Partners of partnerships, as well as prospective partners, are strongly urged to consult with their tax advisors on the potential impact of these rules for any partnership recourse liabilities that arise, or are modified or refinanced, on or after December 2, 2024.

Authors